updated 2/28/2017

Statistical Analysis

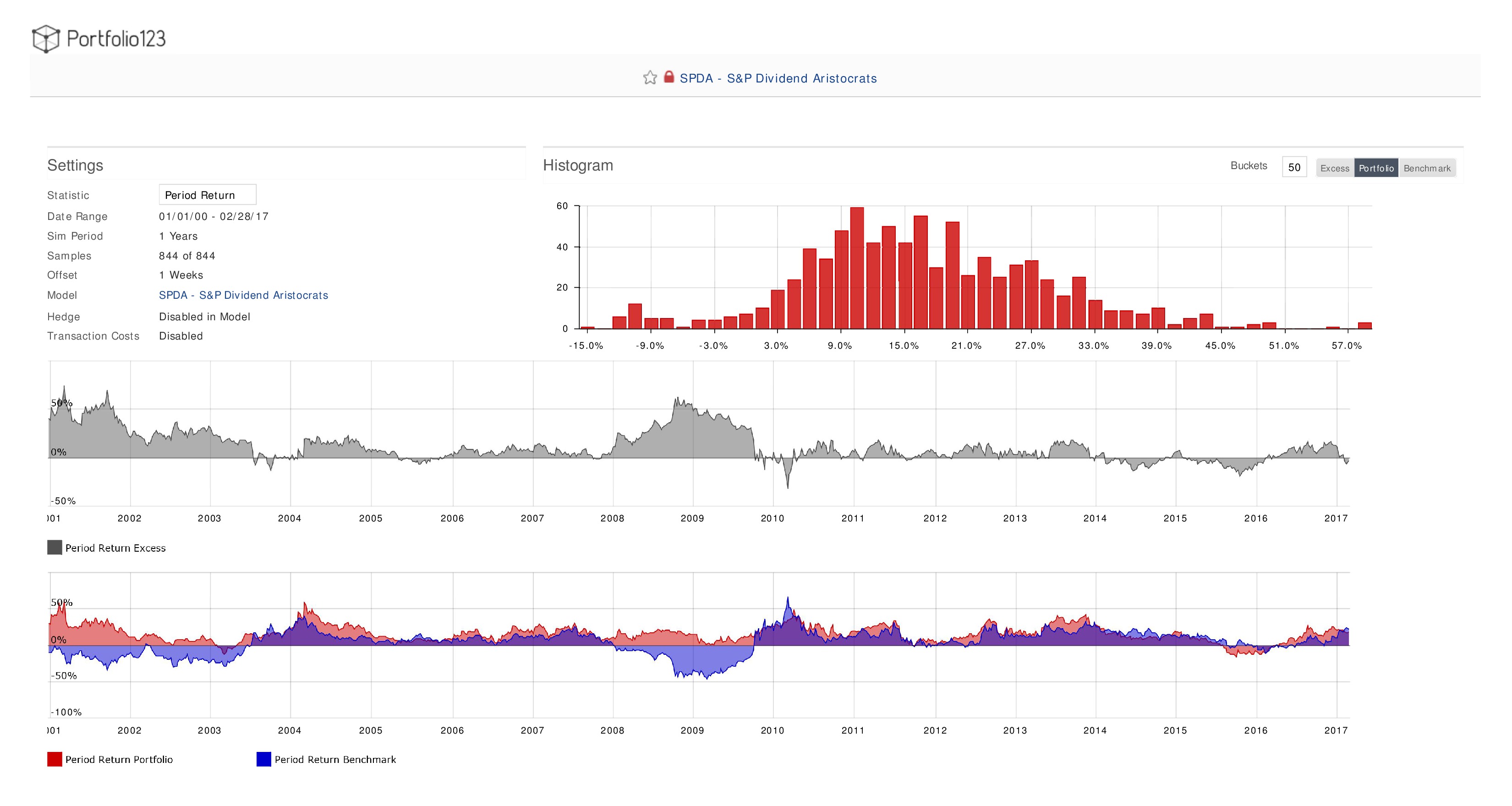

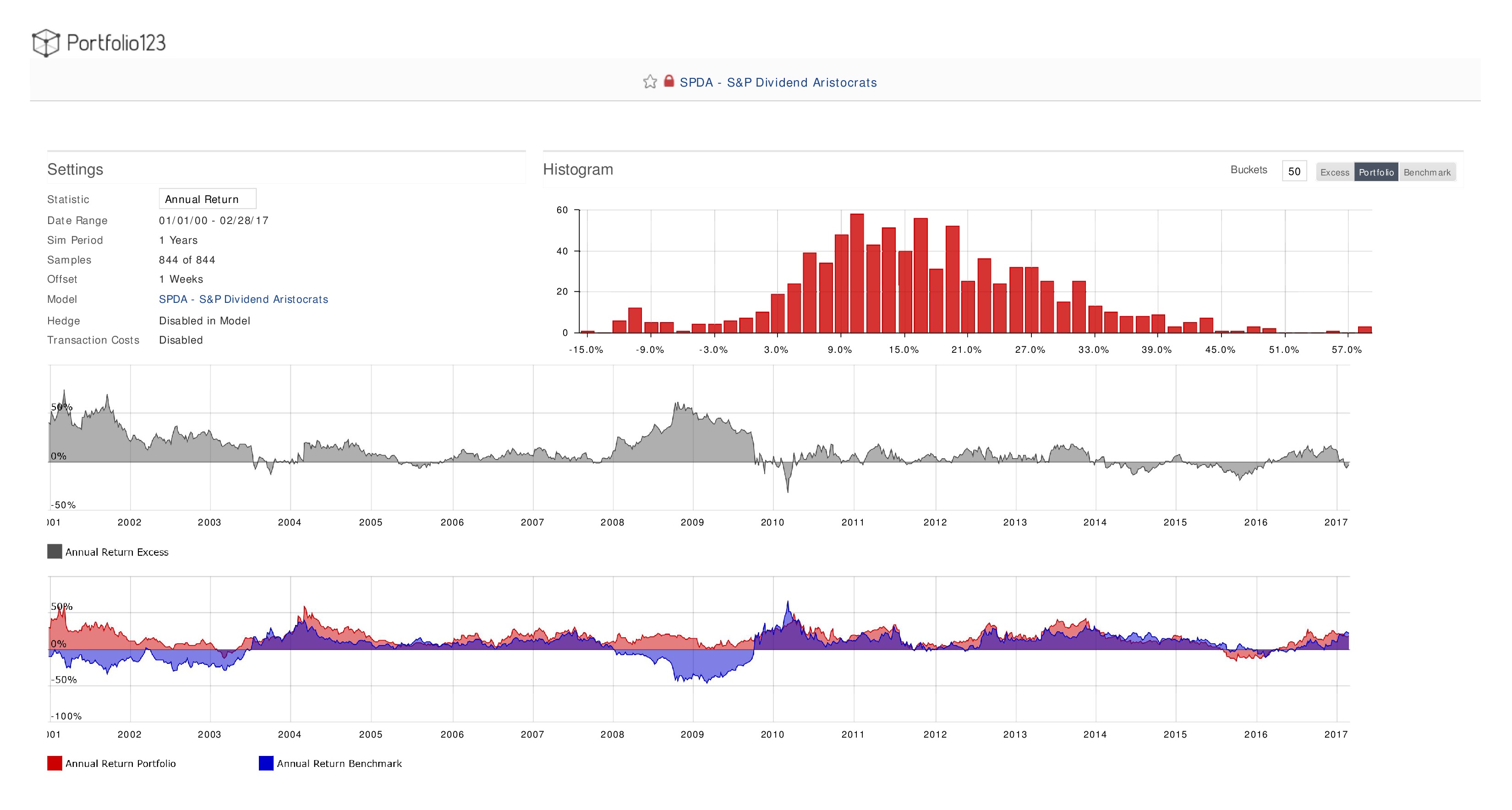

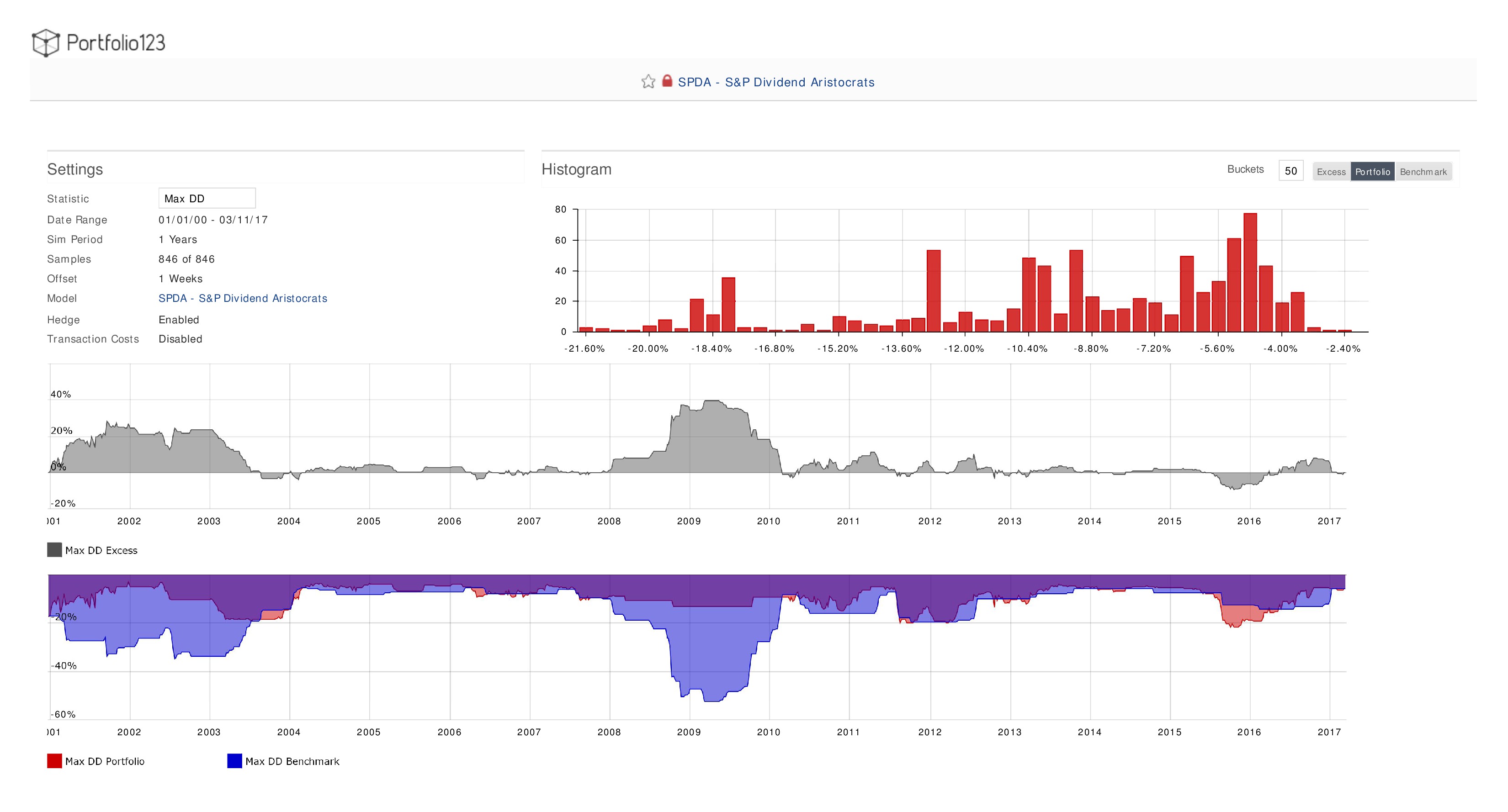

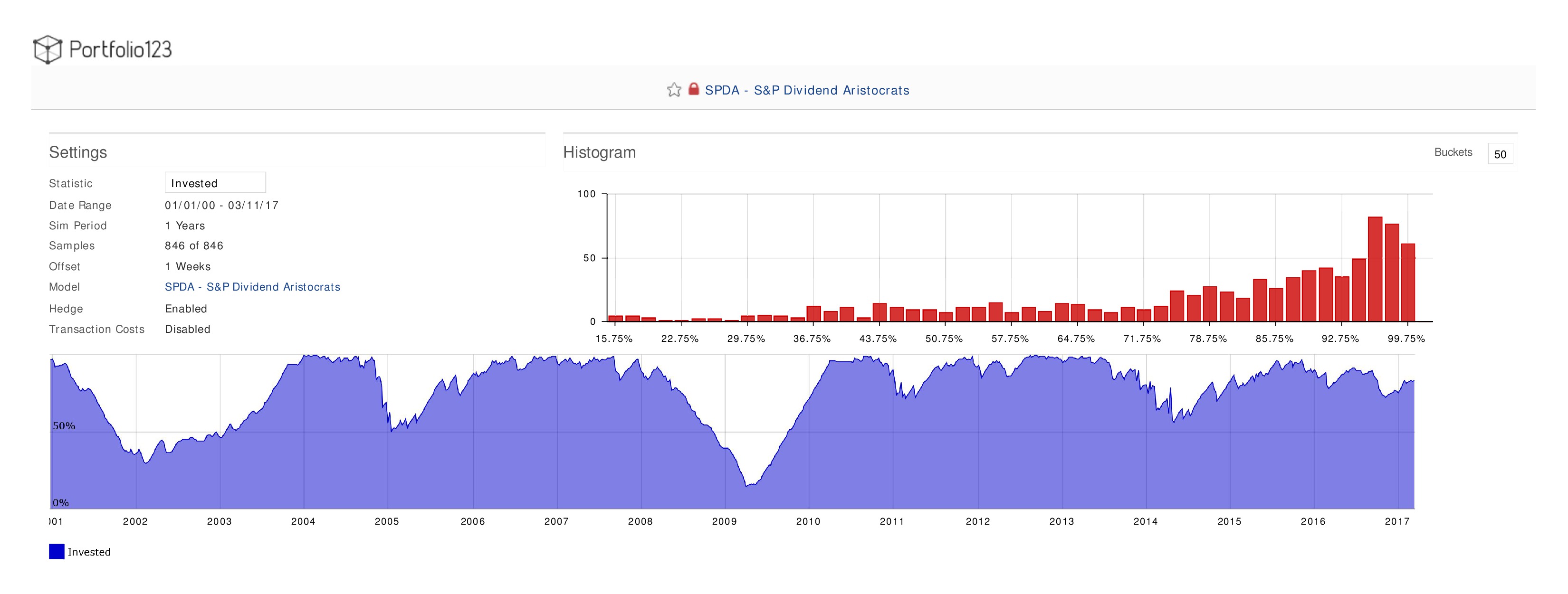

The charts below provide statistical analysis of the model. The charts are created for a rolling 1 year period with a 1 week offset starting with January 1, 2000. The charts are drafted to show 844 fiscal one year rolling returns. More detail will follow to explain each chart.

Period Return

Annual Returns (Similar to Period Returns)

Maximum Drawdowns

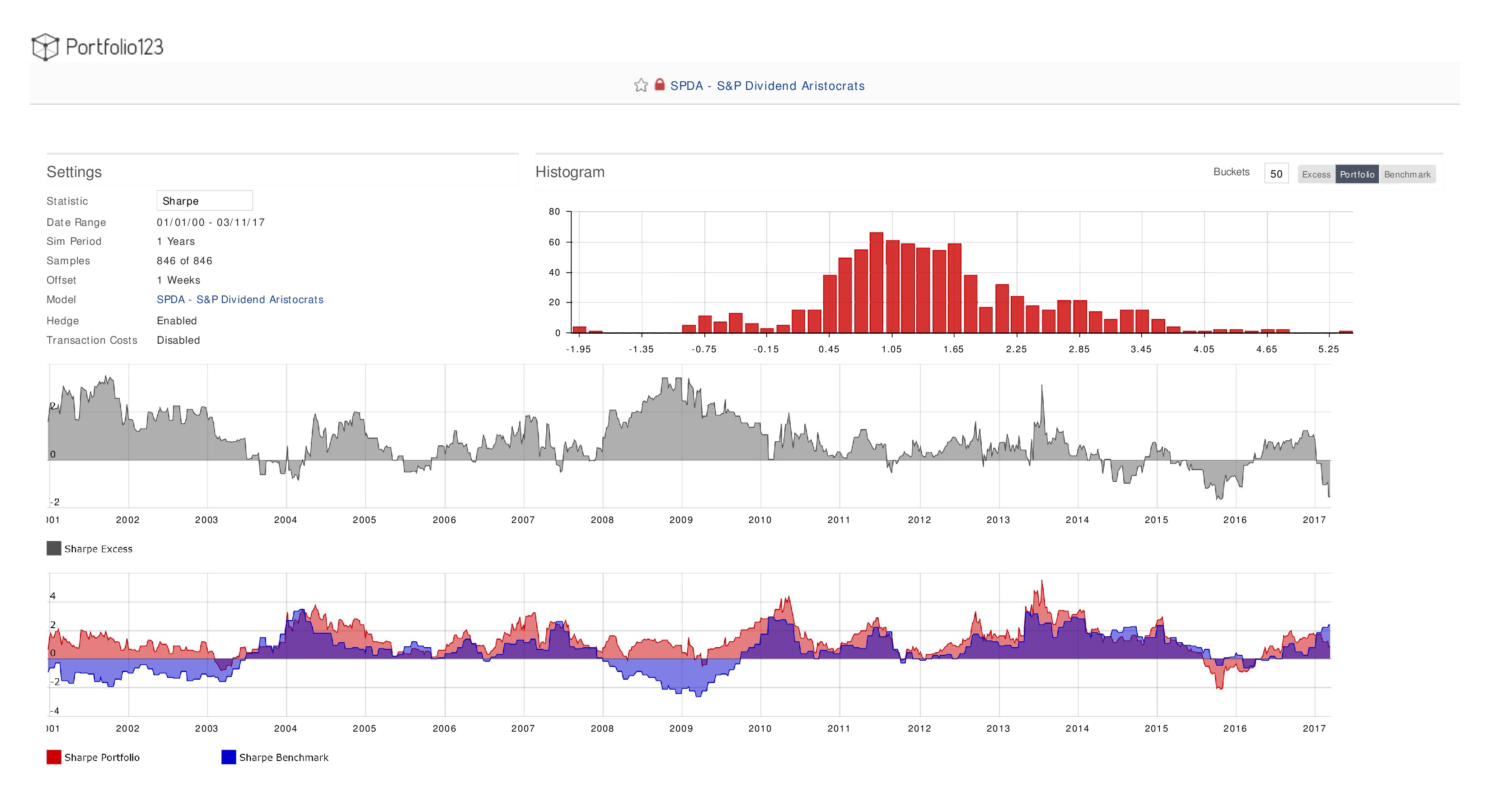

The Sharpe Ratio

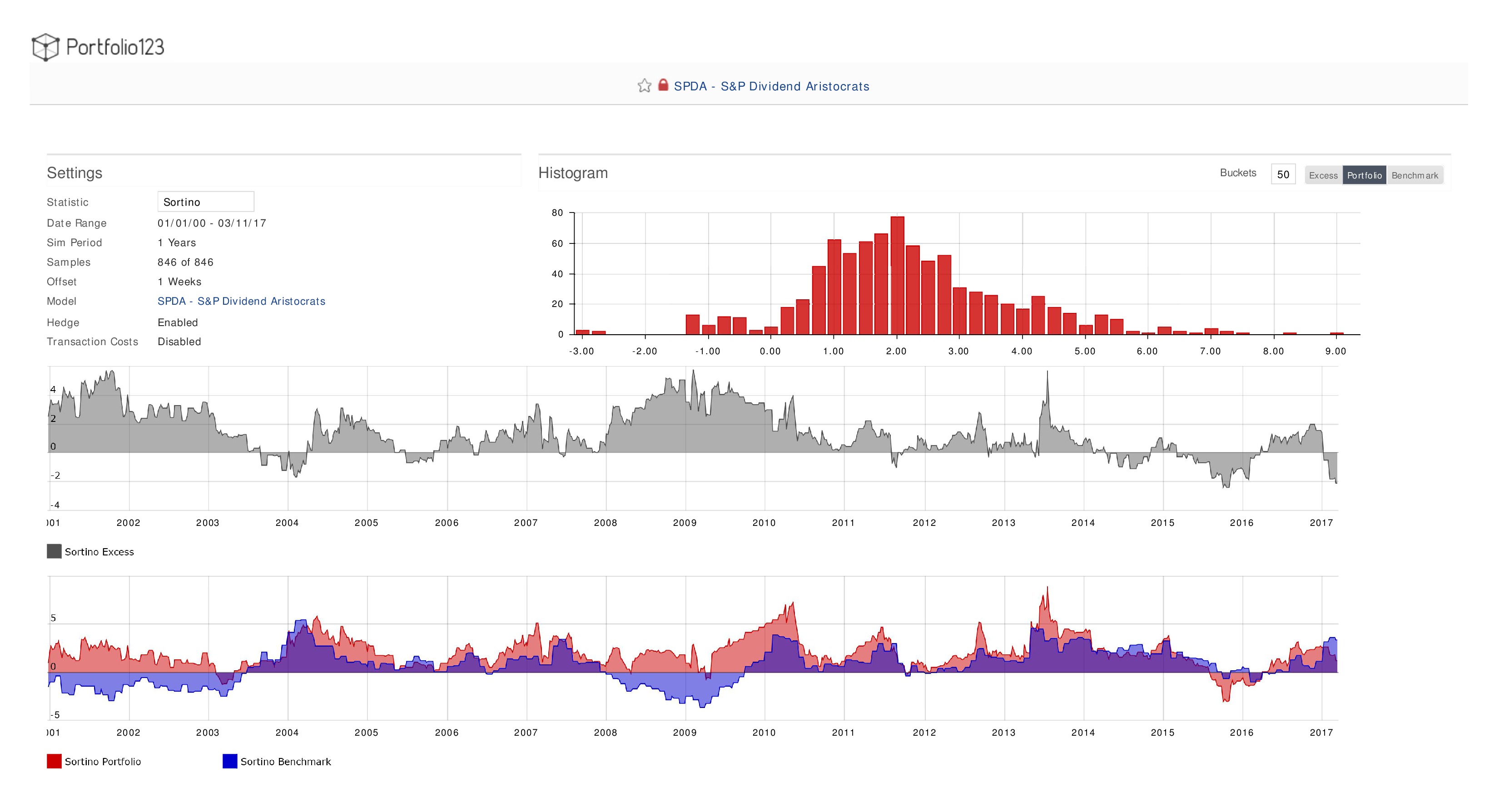

The Sortino Ratio

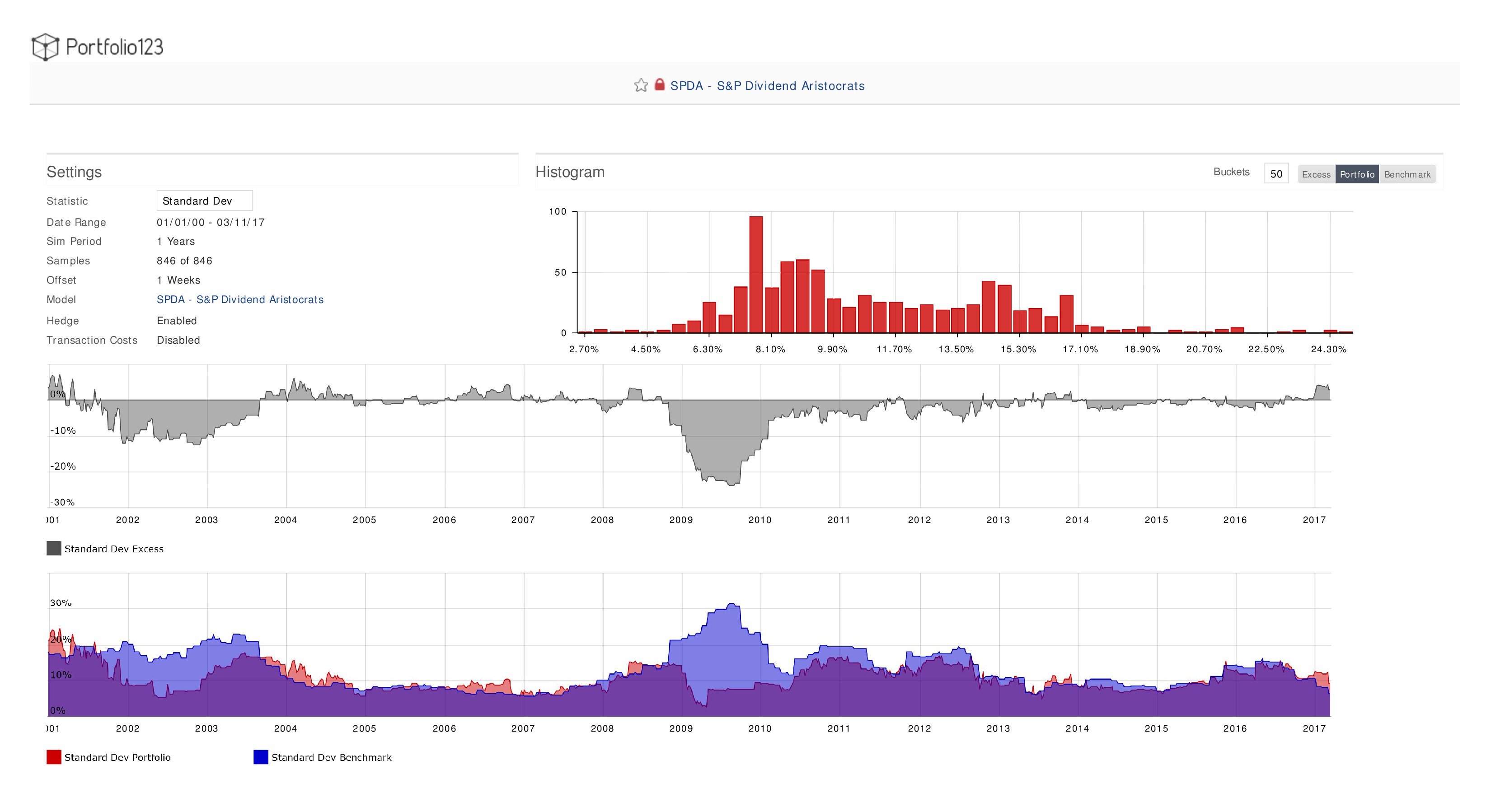

Standard Deviations (Measure of Volatility)

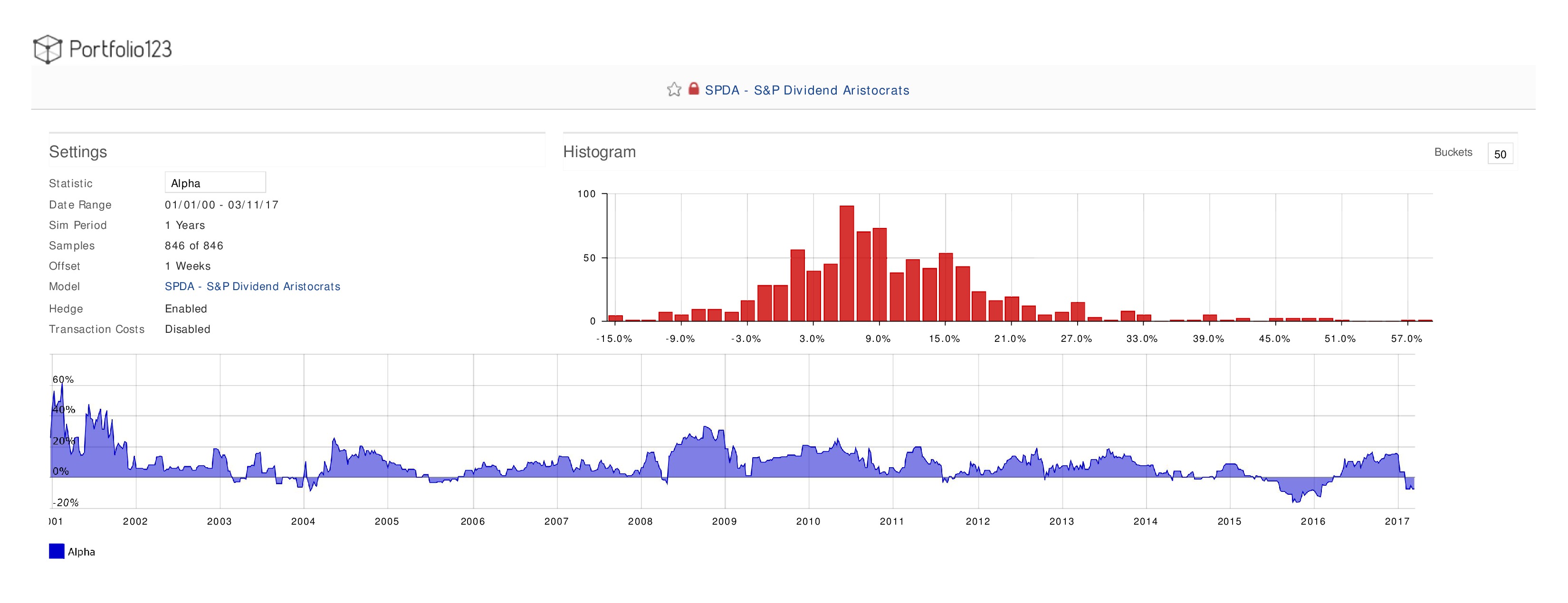

Alpha (the Excess Return vs. S&P 500)

Beta (Volatility vs. S&P 500)

Percentage of Account Invested in Stock Market

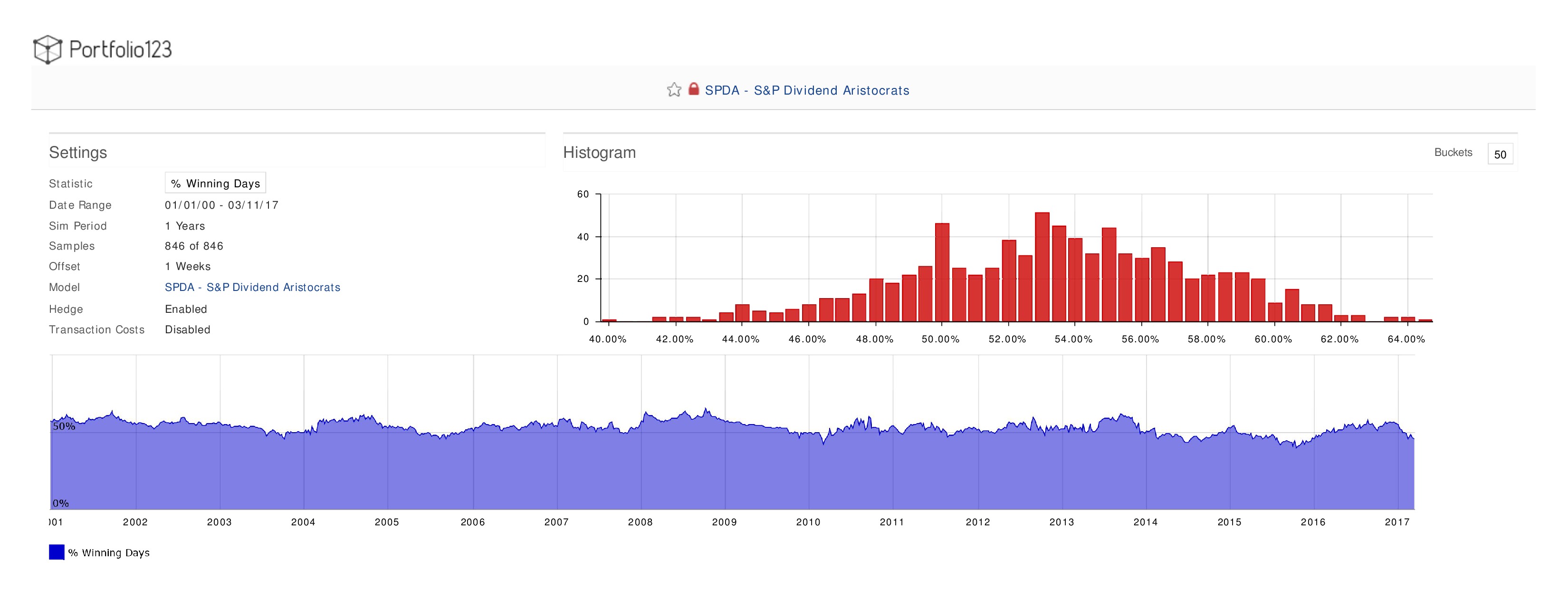

Percentage of Winning Days